- The Nigerian Insurance Industry – A Brief Overview

- Insurance vs Risk

- What is Insurance?

- Definition of Insurance Terms

- A Brief History of Insurance in Nigeria

- Regulatory Framework of Insurance in Nigeria

- Categories (Types) of Insurance

- Key Players in the Nigerian Insurance Industry

- Recent Developments in the Nigeria Insurance Market

- Challenges Facing the Nigerian Insurance Market

- Opportunities in the Nigerian Insurance Industry

- Conclusion

The Nigerian Insurance Industry – A Brief Overview

The insurance industry is one of the oldest components of Nigeria’s financial sector. It is regulated by the National Insurance Commission (NAICOM) and comprises 70 core players (insurance companies), 3 web aggregators, 462 brokerage firms, and several risk adjusters, agents and representatives of the registered companies. While insurance penetration still stands at just 0.5% in Nigeria, there has been remarkable progress lately. Indeed, it has been one of the fastest-growing industries in Nigeria in the past few years. Notably, the industry hit a landmark One Trillion Naira in gross premium generation in 2023. Beyond that, the industry has already generated over 1.173 Trillion as of the third quarter of 2024. It also boasts over 3.88 trillion Naira in assets.

This article is borne out of the need to provide you with reliable information about insurance in Nigeria. It is intended to be a comprehensive guide for anyone who wants to know what insurance is, its history and structure in Nigeria and just about anything. Here, I will also provide you with insider facts for academic research. So, whatever you need, you are at the right place. Let’s dive right in!

Insurance vs Risk

Being comfortable with the concept of risk is crucial to our understanding of insurance. Therefore, we must explore it briefly. A risk is simply the chance that something bad could happen. It is the likelihood or probability of a loss or adverse event occurring, which may result in financial loss or damage to an individual, business, or organization. As Murphy’s law suggests, anything that can go wrong will go wrong.

What is Insurance?

In a word, I would describe insurance as a ‘plan B’ (a backup plan). It is a risk management strategy in which an insurance company (insurer) contractually undertakes to compensate or indemnify a policyholder (insured) against a specified loss, damage, or injury in return for a fee known as a premium. Insurance works like a pool. Picture many people pooling resources, hoping that only a small proportion will have unforeseen needs (claims) within the period. General insurance policies in Nigeria typically last a year.

Definition of Insurance Terms

Every industry typically has some jargons that may sound strange to outsiders. Likewise, insurance professionals employ some terms that may either not be regular English terms or are slightly different from the dictionary meaning of such words. Here, I will focus mainly on the terms I use in this article, as well as some of the most popular terms used in the Nigerian insurance space. See this link for a more complete glossary.

- Insurer – a company that provides insurance services.

- Insured – a person who buys or holds an insurance cover.

- Claim – the value of losses suffered by an insured and covered in the insurance contract.

- Sum insured – the highest amount of cost the insurer can cover for an insured in case of a claim on a non-life insurance.

- Sum assured – The highest amount an insured can claim with regards to life insurance.

- Indemnity – the guiding principle of general business insurance where an insurer undertakes to restore an insured to his previous status before the disaster struck.

Endorsement– a written document that redefines the scope of an insurance policy.

- Compensation – this is the amount typically received by a life policy holder if the claims conditions are met. Since life-related losses cannot be indemnified, the insured is compensated.

- Premium: The amount of money the policyholder pays to the insurance company regularly (e.g., monthly, annually) to maintain the policy.

- Commission – a portion of the premium paid to the broker or agent by the insurance company for facilitating the business.

- BAC – Business Acquisition Cost is a small additional fee paid by the insurance company to the facilitator of the business in lieu of costs incurred in the course of the business

- Underwriting – the process by which an insurance company assesses the risk of providing coverage and determines the appropriate premium for an individual or organization

- Deductible or Policy Excess: The amount of money the policyholder pays out of pocket whenever claim occurs as counterpart to the portion to be covered by the insurance company.

- Policy limits: The maximum amount of money the insurance company will pay for a covered loss. Think of it as the sum insured or assured.

A Brief History of Insurance in Nigeria

Colonial and Precolonial Times

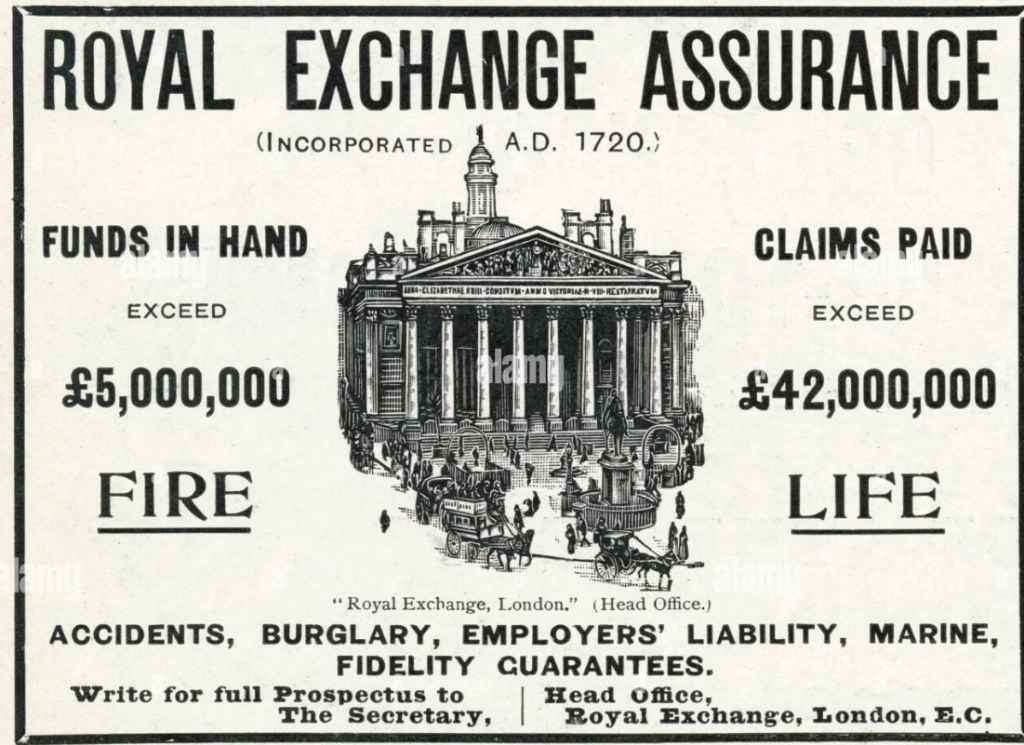

Insurance in its modern form, is often perceived as a Western concept. While some facts about the early practice of insurance in Nigeria are debatable, the British dominated the industry in the late 19th and the first half of the 20th centuries. The Royal Exchange Assurance Company led the way by opening an office in Lagos in 1897, marking the first formal presence of insurance in Nigeria.

Meanwhile, before the advent of the colonialists, Africans had long been engaging in communal risk-managing practices. Even to date, Nigerians still engage in diverse activities that ensure communal support and risk management. An example is a series of rotational resource pooling ventures known as ‘isusu’ or ‘etibe’. Here, members contribute regularly to a pool. The lump sum is then distributed to members in turns, either regularly or in times of need. Also, it was/is a common practice for kith and kin to collectively support any person who faces some form of misfortune or has a major event or project at hand.

Insurance in Nigeria – Post-Independence

Soon after Nigeria gained independence in 1960, the government recognized the need to regulate and develop the insurance sector. Demonstrating its commitment, the government set up a commission headed by J.C. Obande. The commission’s core mandate was to investigate the insurance industry and make recommendations for its future. The Obande Commission among other recommendations led to the establishment of a formal regulatory framework in 1961 – The Insurance Companies Act No. 58 of 1961. This Act mandated the Department of Insurance to regulate the practice. The body was domiciled within the Federal Ministry of Trade. However, it was later moved to the Ministry of Finance.

The indigenization drive of the Nigerian government, especially the Nigerian Enterprises Promotion Decree (NEPD) of 1972 ensured Nigerians took over control of the industry. Before then, almost all the insurance outfits operating within the Nigerian space were appendages or agencies of foreign underwriters. The growth ever since has been phenomenal.

Regulatory Framework of Insurance in Nigeria

The National Insurance Commission (NAICOM) is Nigeria’s primary regulator of insurance practice. The commission was set up by the National Insurance Commission Act 1997. It replaced the Nigerian Insurance Supervisory Board. The Supervisory Board took after the Department of Insurance. NAICOM’s primary responsibility includes ensuring the effective administration, supervision, regulation, and control of insurance business in Nigeria. It also protects insurance policyholders, beneficiaries, and third parties to insurance contracts.

Categories (Types) of Insurance

Insurance policies in Nigeria are categorized into three broad types, defined by the market they serve. These include:

Life Business

This is the assurance of compensation in the event of an occurrence of a defined natural event within the cover period. This insurance cover offers financial protection to individuals and their families in the event of death, disability or critical illness. It specifically deals with life events. Companies operating within the life business segment adopt the term ‘assurance’ because the events covered are mostly certain to occur.

Key Features of Life Assurance

- Life insurance mostly deals with events that are certain to occur.The policies typically last a long period when compared with non-life insurance.Companies offering life insurance typically adopt the term ‘assurance’ as part of their brand name, rather than ‘insurance’.

Products Under Life Business

Life assurance companies offer several policies. Some of them include:

Non-life or General Business

Non-life business, otherwise called general business is a contract of indemnity between an insurer and an insured where an insurance company undertakes to restore the insured to his original position before an unforeseen loss occurred. Unlike life business, general insurance protects the insured’s assets against losses. It is not designed for the insured to profit from the cover, but to recover his pre-loss state.

Key Features of General Insurance

- The policies typically last for a year or less.

- No premium, no cover as prescribed by NAICOM.

- Guided by the principle of indemnity.

- Unlike life insurance, general insurance policies do not offer any maturity benefits. If no claim is made during the policy term, the premium paid is not returned to the insured.

- The premium paid for a general insurance policy is determined by the level of risk involved. Factors that influence the premium include the type of coverage, the value of the insured asset, the location, and the insured’s claims history.

Products Under the Non-life Business Segment

These are some of the products offered by general business insurance companies. For a more complete list, click here.

Reinsurance

Reinsurance companies are in business to insure insurance companies. They are a critical part of the insurance industry. They ensure stability and allow insurance companies provide coverage even for the largest and most complex risks.

Key Features of Reinsurance Companies

- They reduce the risk of bankruptcy and promote the profitability of insurance companies.

- They primarily serve insurance companies.

Products Offered by Reinsurance Companies

- Facultative reinsurance: Coverage for a specific individual risk.Treaty reinsurance: An ongoing agreement covering a portfolio of risks.Proportional reinsurance: The reinsurer shares a proportionate amount of the premiums and losses with the insurer.Non-proportional reinsurance: The reinsurer covers losses above a certain threshold.

Other Service Categories

Microinsurance

NAICOM published the uniform guideline for microinsurance operations in Nigeria on 1st January 2018. The guideline defines microinsurance as “insurance products that are designed to be appropriate for the low-income market, low-valued policies, micro and small scale enterprises in relation to cost, terms, coverage, and delivery mechanism”. The prevailing economic situation and the low penetration of insurance occasion the rising importance of microinsurance in Nigeria. The role of microinsurance companies in the penetration drive cannot be overstated as most Nigerians only own assets that fall within the scope of microinsurance.

Scope of Microinsurance

Below is the scope defined by NAICOM’s guidelines.

Takaful insurance

Takaful insurance is widely known as Islamic insurance. It is a form of insurance that incorporates elements of mutuality and ethical finance considerations and is open to all people regardless of faith and background. See our article on Takaful insurance for more.

Key Players in the Nigerian Insurance Industry

Insurance companies

Insurance companies are the most fundamental players in Nigeria’s insurance industry. There are seventy-three insurance companies, categorized based on their product offerings and the market they appeal to. These companies are as follows:

Brokers

Insurance brokers play an important role in the Nigerian insurance market. They are intermediaries between the insured and insurers and account for as much as 70% of insurance businesses done in Nigeria. They are 462 registered insurance brokers in Nigeria.

Insurance Agents

Agents as the name implies are representatives of insurance companies who are authorized to enter contractual relationships on behalf of the principal company. While agents and brokers may seem alike, there are clear differences between them. See this article on the difference between insurance brokers and agents.

Web Aggregators

Insurance aggregators are digital platforms where insurance products can be bought and sold. A web aggregator according to NAICOM, is a company that owns or maintains a website and avails information on insurance products and prices, features comparisons of products of different insurers and offers leads to an Insurer. There are three licensed web aggregators.

Loss Adjusters

Loss adjusters are independent professionals retained by insurance companies to investigate and assess the extent of damage or loss when a policyholder makes a claim. An adjuster inspects accident scenes, evaluates claims incidences, determine the cause and extent of a loss or damage, negotiates payouts and recommend a fair settlement to the insurer. It is the industry practice to use a loss adjuster who is expected to be somewhat neutral.

NAICOM

The National Insurance Commission is the primary regulator of the insurance industry in Nigeria. Its key roles can be summarized as follows.

Other Organizations

Some powerful bodies that influence insurance operations in Nigeria include:

Recent Developments in the Nigeria Insurance Market

- Compulsory Third Party Motor Insurance Enforcement: The Inspector General of Police announced the enforcement of compulsory third party from February 1, 2025.

- Nigeria Insurance Industry Reform Bill, 2024: The Senate Committee on Banking, Insurance and other Financial Institutions chaired by Senator Tokunbo Abiru passed this bill which seeks to increase the capital base of insurance companies. It provides for N25 billion for Non-life Assurance, N15 billion for Life Assurance and N35 billion for Reinsurance firms.

- Recapitalization Fears: The National Insurance Commission (NAICOM) has been pushing for the recapitalization of insurance companies to increase their capacity and improve the industry’s financial stability. This has led to mergers, acquisitions, and consolidation in the industry.

- Digitalization: There’s a growing adoption of technology and digital tools by insurers to improve operational efficiency, customer service, and product delivery. This spans online sales, mobile apps/chatbots, and claims processing.

- No-premium-no-cover: The enforcement of this policy has helped stabilize and improve transparency in the industry.

- 1 trillion Naira Premium: The insurance industry in 2023 celebrated hitting the one-trillion mark.

- Motor Insurance premium review: NAICOM in 2023 reviewed the premium for motor insurance. This has increased profitability within that segment.

- NIID: The introduction of the Nigerian Insurance Industry Database contributed to checking fraud by providing an independent platform for the verification of policies.

- NIIP: NAICOM in 2024 introduced the Nigerian Insurance Industry Portal, a central portal for buying and selling third party motor insurance.

Challenges Facing the Nigerian Insurance Market

- Low insurance penetration: Insurance adoption is still less than 1%.

- Lack of trust and awareness: The negative experiences of the past still linger in the minds of Nigerians.

- Economic downturn: Nigerians are facing some of the worst economic situations ever. With many businesses closed and citizens pushed into poverty, there is little to insure.

- Fraud and unethical practices: The activities of fake insurance agents impact the industry negatively.

Opportunities in the Nigerian Insurance Industry

After a period of sustained downturn, the Nigerian economy is showing signs of recovery. While there may be limited correlation between the growth in the real sector and insurance, it is certain that they have an almost proportional relationship at least to an extent. Hence, with the real sector expected to grow, one can expect an increase in demand of insurance.

Beyond this, the rise in technology and innovation is pushing the bounds of insurance in Nigeria. New players like insuretech and aggregator platforms are revolutionizing the industry. Also, the advancement in AI and big data is bound to drive profitability and efficiency. Finally, government initiatives aimed at deepening adoption and penetration like compulsory covers make the long term prospect of the industry very positive.

Conclusion

The Nigerian insurance industry is a growing sector with immense potential. However, it faces significant challenges. Despite a large and youthful population, insurance penetration remains low, hindered by factors like low awareness, affordability and a lack of trust. That said, the industry is showing resilience, driven by a growing middle class, increasing regulatory reforms, and the adoption of technology.

2 thoughts on “Insurance in Nigeria: All You Need to Know in 2025”